Has The Rupee Depreciation Derailed India's Investment Story?

You invest $1 million in Indian equities. Over the next year, the rupee falls 3-5%. Did you just lose money?

This is the first question most U.S. investors ask about India exposure. It’s a fair concern—especially in 2025, when the rupee weakened while several other emerging market currencies strengthened.

But long-term data tells a different story: rupee depreciation has been persistent, yet it has not prevented strong dollar equity returns.

The Rupee in Historical Context

Since 1995, the rupee has moved from roughly ₹31 per dollar to around ₹90 — an average depreciation of about 3–3.5% annually.The rupee’s depreciation has been measured, predictable, and importantly, controlled to a large extent by a credible central bank with substantial reserves. Unlike peers such as Turkey, Argentina, or Brazil, India has avoided disorderly collapses. The rupee’s path has been steady, not chaotic.

Why the Rupee depreciates

The rupee depreciation reflects the following economic factors:

1. Inflation

Higher inflation driven by higher growth naturally lead to currency adjustment. According to Purchasing Power Parity theory, exchange rates adjust over time to reflect differences in inflation between countries.

The historical inflation gap between the U.S. and India has begun to narrow. As India strengthens its control over inflation, the differential is gradually declining—suggesting that the pace of future rupee depreciation may moderate over time.

2. Current account deficit

Like many fast-growing economies, India runs a trade deficit—importing more goods than it exports—which increases demand for U.S. dollars and places gradual downward pressure on the rupee.

5. Managed float framework

The RBI allows orderly currency movement rather than defending artificial exchange rate levels — reducing the risk of sudden devaluations that erode confidence and destroy capital.

The key point: depreciation has reflected growth and macro adjustment, not instability.

The Only Return That Matters For U.S. Investors: USD Returns

For U.S. investors, only one metric matters: dollar returns

21-year track record (2004-2024)

- Sensex performance in Rupee terms: 13.6% CAGR

- INR depreciation: ~3.1% annually

- USD-adjusted Sensex returns: ~10.5% CAGR

- S&P 500 : ~8.6% CAGR

Sources: Sensex data from BSE/NSE archives; S&P 500 data from Official Data/Macrotrends; Currency data from RBI/Investing.com

Even after currency depreciation, Indian equities delivered positive dollar returns that compared favorably with developed market alternatives. Additionally, for the same period, returns including dividends for S&P was 10.6% while the Sensex was 11.6% (14.7% in rupee terms) Thus, despite the currency depreciation, Indian equities produced dollar returns higher than the S&P 500.

But here’s where you’ll find the clear alpha - intelligent stock picking!

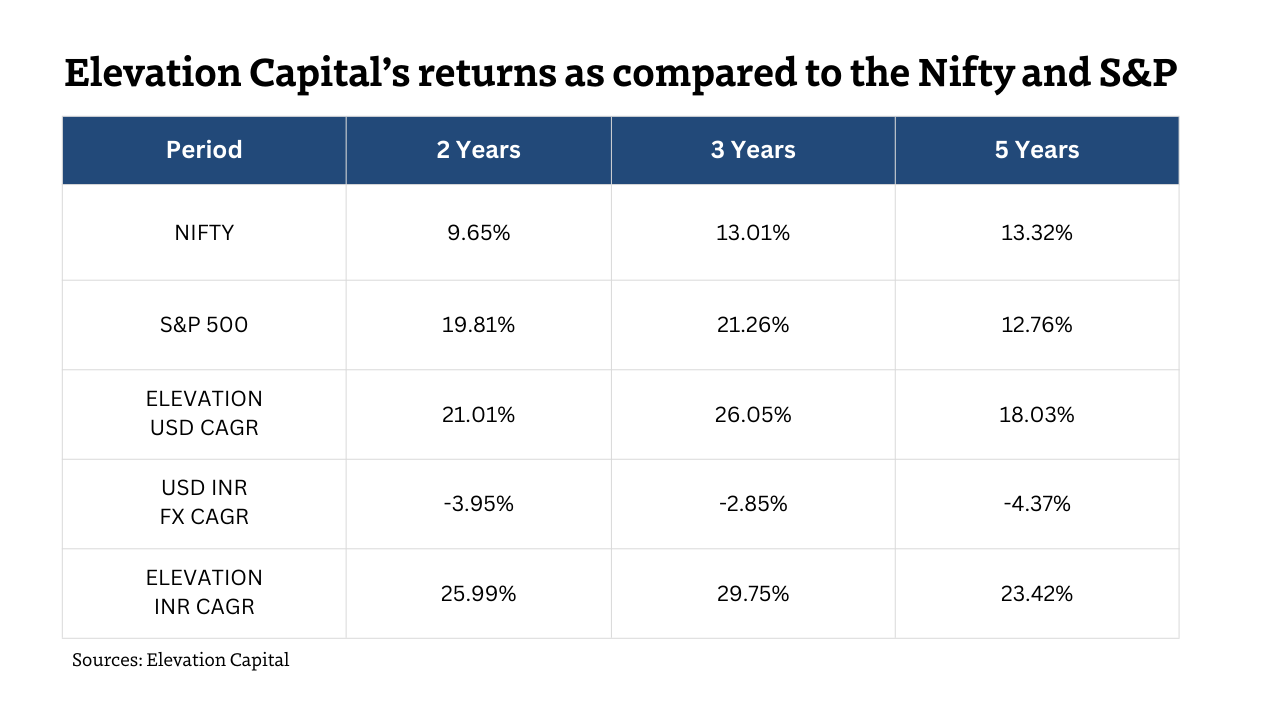

Below is a table comparing Elevation Capital’s returns as compared to the Nifty and S&P.

Indices like the Nifty do not represent the investment opportunity in India. They tend to hide the large dispersion in a market as dynamic as India, which rewards stock pickers and active management!

Elevation’s performance demonstrates that stock selection—not currency—is the primary driver of long-term returns in India.

Despite the rupee depreciating at roughly 3–4% annually, Elevation has compounded at:

- 26.05% (3-Year USD CAGR)

- 18.03% (5-Year USD CAGR)

This represents a substantial outperformance over the S&P and the India Nifty USD index.

The takeaway is clear: superior stock selection in India can more than offset currency headwinds.

Currency Depreciation and Equity Returns: Why India’s Weak Currency Did Not Prevent Strong Dollar Returns

A common investor concern is that currency depreciation erodes returns. While true short-term, the long-term relationship is more complex.

Since 2005, the Indian rupee depreciated ~3.5% annually (44 to 90 per USD), while the Chinese yuan remained stable. Logic suggests Chinese equities should outperform. The opposite occurred.

Actual Returns (USD, 20 years):

- India: ~10.5% CAGR

- China: ~6% CAGR

- S&P 500: ~8.5% CAGR

Currency depreciation in India has largely reflected inflation differentials and external trade balances. Rather than forcing deflation by increasing interest rates or causing credit contraction, the exchange rate absorbed macro adjustments.

This policy had an important consequence: corporate profitability was protected.

Indian companies maintained pricing power. Exporters became more competitive. Corporate profitability continued to compound—even as the rupee weakened.

China followed a different model. The yuan was tightly managed in the name of macro stability, but much of the country’s GDP growth flowed to infrastructure, state-owned enterprises, and policy objectives rather than minority shareholders. As a result, earnings per share grew far more slowly than headline economic growth.

The contrast highlights an important factor for foreign investors: Dollar equity returns = Local earnings growth − Currency depreciation.

In India, earnings growth more than offset currency weakness. In China, currency stability couldn’t compensate for weaker per-share profit growth.

Over the long run, equity markets reward the share of growth captured by corporate profits—not exchange rate stability. India’s experience proves it: the rupee weakened, but earnings compounded, and dollar returns remained strong.

The lesson for investors—currency moves affect short-term outcomes; earnings growth drives long-term returns.

Our view

Stock selection matters more than currency for long-term investors! Currency depreciation is a factor in our analysis, not the factor. Over multi-year periods, equity selection, portfolio construction, and the strong economic tailwinds in India dwarf currency impacts. Demographics, digitalization, formalization, infrastructure, and institutional stability are fundamentals that transcend currency movements.

“The currency headwind exists, but the growth tailwind dominates”

Every successful emerging market investor has navigated currency depreciation while capturing economic transformation.

The question is not whether the Indian Rupee will continue to adjust - history suggests it might be roughly 3% annualized.

The Chinese yuan depreciated at an average rate of 5.2% annually in the 20 year period between 1985 and 2005 before stabilizing in the last 20 years.

The real question is whether earnings growth will more than compensate.

In India, over the past two decades and longer, it has.

“If rupee depreciation is your biggest worry about investing in India, you're not focused on the right risks.”

The real issues are successful execution of growth oriented economic and social policies, continuity of reforms and geopolitical stability.

Currency depreciation is the cost of accessing a high-growth economy. Based on long-term evidence, it has been a cost worth paying.

And we’re aligned with that conviction. Elevation operates with a no management fee and 6% USD hurdle rate—we earn fees only after overcoming currency headwinds. If we weren’t confident that disciplined stock selection in India can generate returns well above that threshold, we wouldn’t structure our economic outcome around it.

%20copy.png)