India’s Consumption Revolution: A Structural Investment Opportunity

A Market in Motion

India is already the world’s fifth-largest consumption market—but the headline ranking understates the velocity of change. Between 2013 and 2024, private consumption nearly doubled, growing at a compound annual growth rate (CAGR) of 7.2%, outpacing developed economies like the U.S., Germany, and even China.

And this is only the beginning. By 2026, India is projected to emerge as the world’s third-largest consumer market, powered by structural shifts that are redefining its economic trajectory.

The Income Revolution: Driving Discretionary Demand

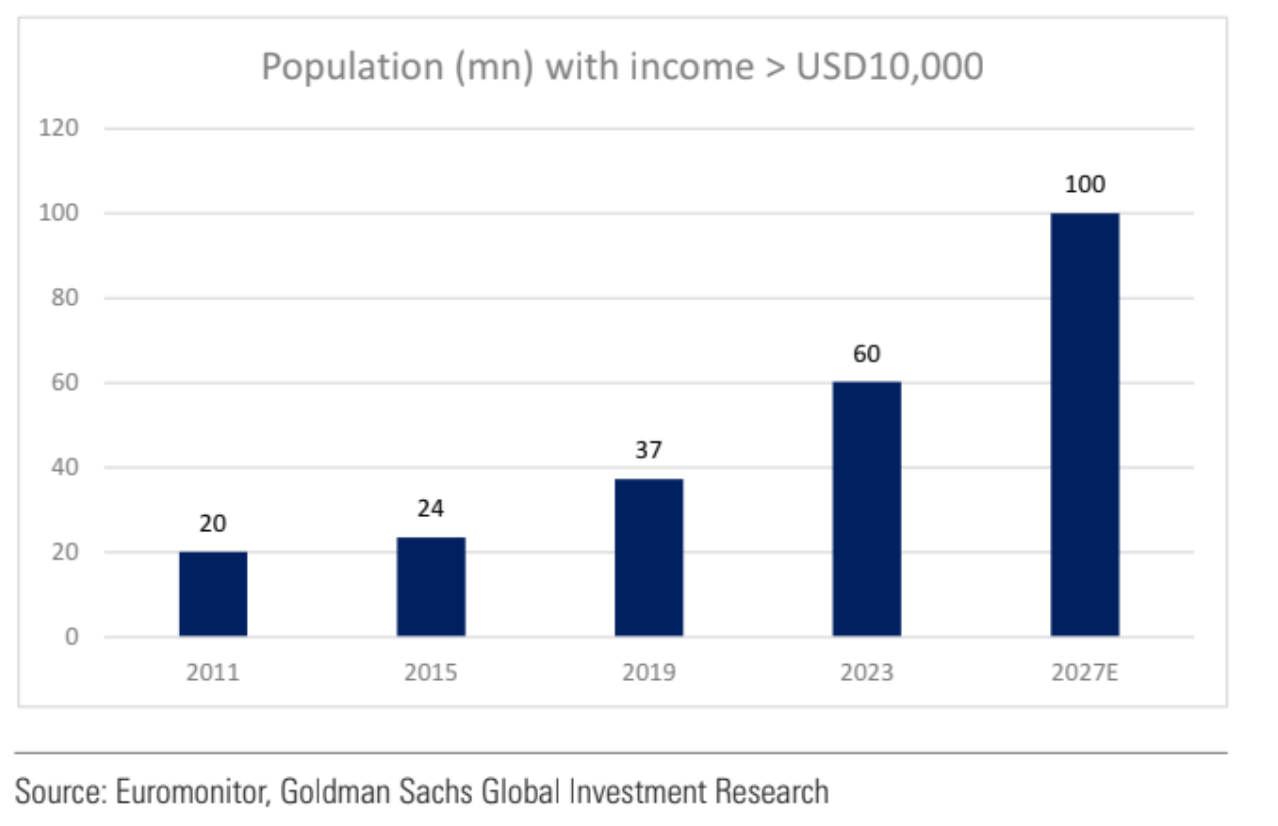

At the heart of this shift is rising affluence. Over the past decade, India’s per capita income has more than doubled—lifting tens of millions into the consuming class and shifting purchasing patterns across the board. What was once a market dominated by essential spending is now increasingly tilted toward discretionary, premium, and experiential consumption.

Goldman Sachs estimates that India will have over 100 million affluent individuals—earning more than $10,000 annually—by 2027. This affluent class is driving a trend economists refer to as “premiumization”—a decisive move away from price sensitivity toward quality, brand, and convenience.

Consider the Coldplay concert in Mumbai: tickets released via BookMyShow saw 13 million users in the virtual queue, selling out within 60 minutes. This wasn’t merely entertainment—it was a reflection of India’s emerging experience economy, where status is increasingly associated with how people spend their time, not just their money.

The Great Consolidation: From Unorganized to Organized

Parallel to rising incomes, India is witnessing a significant transition from informal to organized retail. Sectors such as jewelry, real estate, electricals, and FMCG are consolidating rapidly, with publicly listed, professionally managed businesses capturing share from unorganized players.

This shift is structural—not cyclical—and presents a long-term investment thesis. As scale, branding, and supply chain efficiency become differentiators, organized players are positioned to generate disproportionate returns on capital and compound shareholder wealth.

Q-Commerce: The New Standard in Consumer Expectations

India has done something few global markets have: mainstreamed Quick Commerce (Q-commerce). From groceries to gadgets, products are delivered in 10–20 minutes—a radical shift from the one-day delivery once considered fast.

While Q-commerce models have struggled for scale in Western markets, India’s success stems from a unique combination of factors:

- Dense urban clusters

- Lower delivery costs

- Digital payment infrastructure (led by UPI)

- AI-powered logistics and GPS optimization

According to Datum Intelligence, India’s Q-commerce market is expected to grow from $6.1 billion in 2024 to $40 billion by 2030, at a staggering 48% CAGR—making it the fastest-growing retail channel in the country.

More than just speed, Q-commerce platforms now possess hyperlocal consumer data, which is fueling the rise of digital-native and D2C brands. These brands bypass traditional offline distribution channels to serve India’s 30 million affluent households with tailored, premium products.

Underpenetrated Markets: A Long Runway for Growth

Despite the growth, many sectors remain significantly underpenetrated—suggesting ample room for expansion. The numbers are revealing:

- Only 3% of the population has a formal credit card

- Just 3% invest in mutual funds

- Insurance penetration stands at 4.2% of GDP (3.2% life, 1.0% non-life)

- Roughly 30 million households own a car

- Only 8% of India’s 300 million households have air conditioners

These are not just statistics—they are signals of latent demand. As income levels rise, credit expands, and financial literacy improves, these categories are poised for explosive growth.

The Digital Stack: India’s Infrastructure Advantage

The rise in consumption has been catalyzed by India’s digital infrastructure—particularly the Unified Payments Interface (UPI), which processes over 10 billion transactions monthly. UPI, combined with Aadhaar, Jan Dhan bank accounts, and mobile penetration, has democratized access to products and services that were once out of reach.

This has enabled a bottom-up consumer revolution. Even Tier 2 and Tier 3 cities are now meaningful contributors to e-commerce, digital finance, and Q-commerce.

Consumption and GDP: A Virtuous Cycle

Here lies the most powerful tailwind: private consumption accounts for nearly 60% of India’s GDP. Unlike export-led economies, India’s growth engine is largely domestic. As consumption rises, it fuels GDP growth—which in turn creates more income, more spending, and more investment opportunities.

This feedback loop makes India’s consumption story not just a sectoral theme, but the core driver of the country’s economic ascent.

The Investment Case: A Market Up for Grabs

India’s consumption revolution offers multi-decade investment potential across a wide spectrum:

- Large, listed players consolidating fragmented markets

- Digital-native brands leveraging new platforms and behavioral shifts

- Financial and lifestyle services moving from low to high penetration

- Infrastructure and technology businesses enabling this ecosystem

This convergence of demographics, digitization, and economic transformation positions India as a consumption-led economy in a league of its own.

Time to Participate

The story of India’s consumption is still unfolding. For investors, the question is no longer if they should participate, but how swiftly they can position themselves to capture the opportunity.

This is not merely a growth narrative — it represents a structural re-rating of how 1.4 billion people consume, aspire, and build their futures. For those who recognize the underlying forces at play, the chance to participate in decades of compounding is not sometime in the future — it is here, and it is now.

%20copy.png)