India’s Journey from a Nation of Savers to a Nation of Investors

The Shift Toward Financialization

Financialization refers to the growing movement of household savings from physical assets like gold and real estate toward financial instruments such as mutual funds, equities, and bonds. Historically, the average Indian household parked wealth in bank deposits or tangible assets like gold and real estate, often shying away from capital markets due to distrust, lack of access, or limited financial literacy.

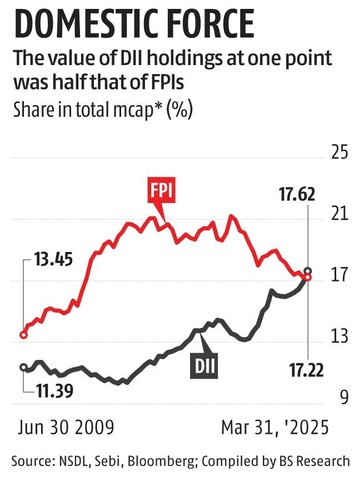

This long standing skepticism toward equities had an interesting side effect: for many years, foreign institutional investors (FIIs) held more Indian equities than domestic investors. India’s markets, in turn, were highly sensitive to global capital flows, with foreign sentiment often driving market direction.

A Structural Breakthrough

That reality has now shifted. In a significant development, domestic investor ownership in Indian equities has surpassed foreign holdings. Just ten years ago, foreign ownership was nearly double that of domestic investors. Today, Indian retail investors—empowered by better access, digital infrastructure, and rising financial literacy—are emerging as a dominant force in capital markets.

The implications are profound. This transition signals a structural change in market behavior. With a stronger domestic investor base, India’s equity markets are becoming less vulnerable to global volatility and external shocks. Investor sentiment is increasingly being shaped by local factors rather than events in the West.

Retail Money as a Stabilizing Force

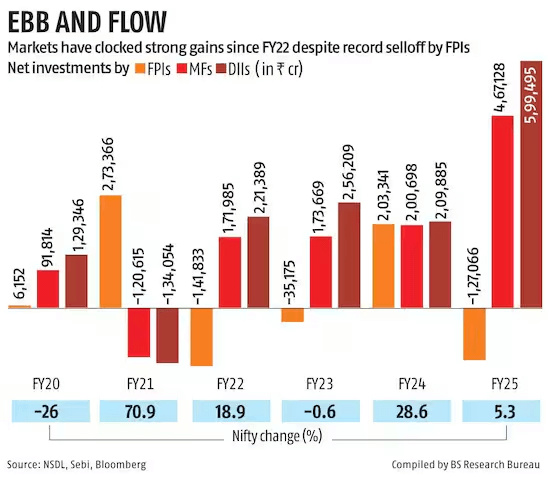

A prime example came in October 2024, when foreign investors pulled out over ₹1 trillion from Indian markets. In the past, such an event would have triggered a sharp market correction. But this time, domestic investors stepped in with equal force, stabilizing prices and acting as a shock absorber during turbulent times.

The resilience of retail investors shows the growing maturity of India’s stock market and its ability to decouple from international capital flows.Much of this resilience is being driven by the surge in retail participation through Systematic Investment Plans (SIPs)—monthly, automated investments into mutual funds.

India’s Investing Revolution Backed by Hard Numbers

The scale of India’s financialization is not just visible anecdotally—it is backed by hard data.

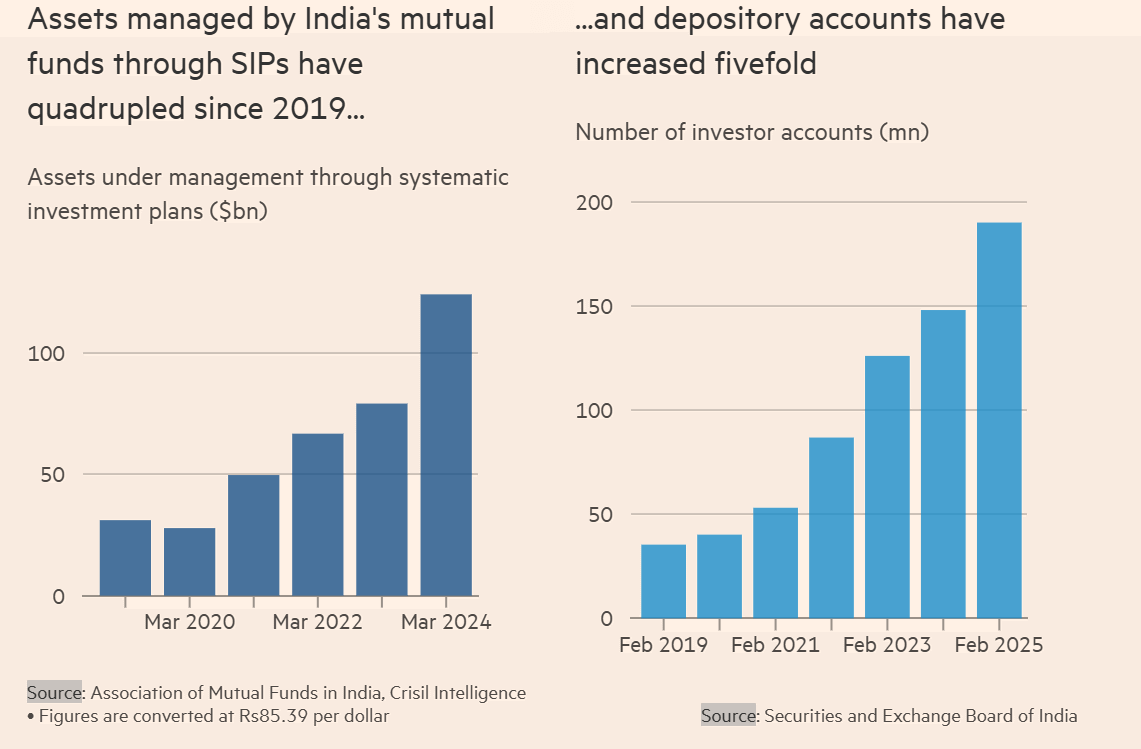

According to the Association of Mutual Funds in India (AMFI), the amount of money managed through Systematic Investment Plans (SIPs) quadrupled to $124.3 billion between 2019 and 2024. This explosive growth reflects how SIPs have become the preferred vehicle for retail investors seeking disciplined, long-term exposure to equities.

At the same time, the number of demat (depository) accounts—required to hold and trade securities—quintupled to 190 million, according to the Securities and Exchange Board of India (SEBI). This indicates an unprecedented surge in retail participation and formal integration into capital markets.

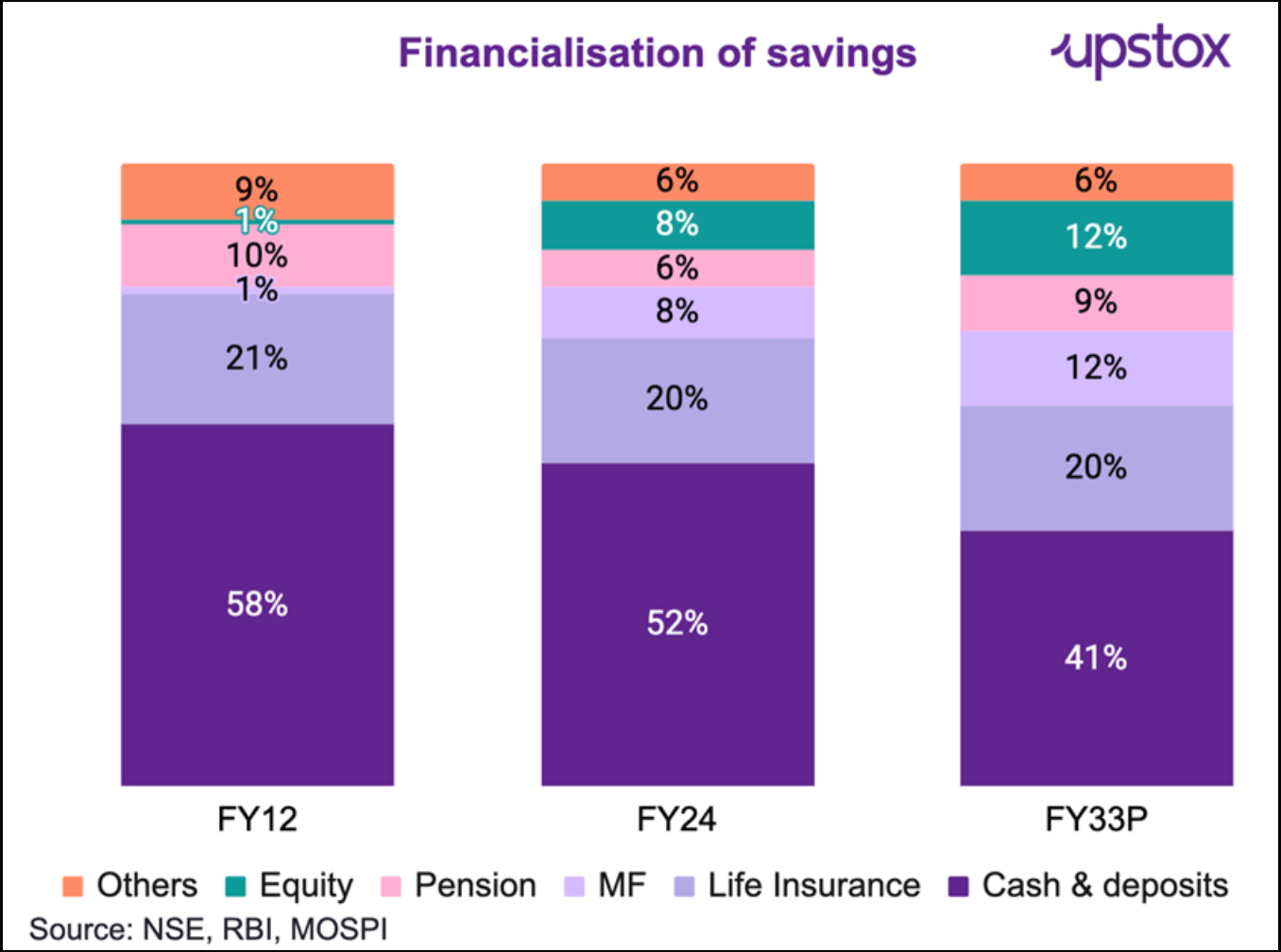

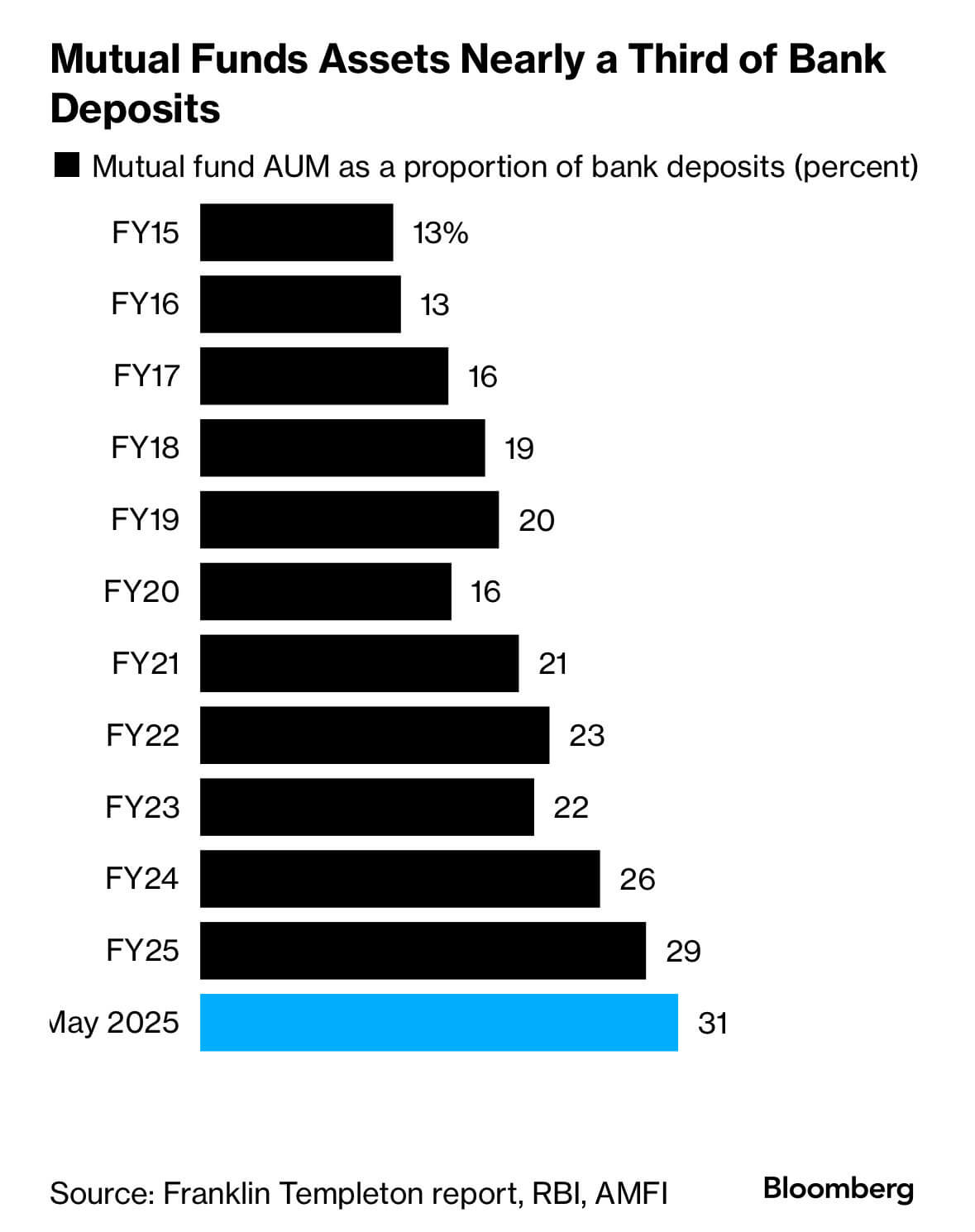

What’s even more telling: mutual fund assets under management (AUM) grew at a faster rate than bank deposits over the same five-year period. This marks a fundamental behavioral shift—from passive saving to active investing—as more Indians seek returns beyond traditional bank products.

Together, these metrics point to a pivotal transformation in the financial landscape of India—one where households are taking charge of their financial futures through transparent, regulated, and growth-oriented financial products.

Digital Rails Enabling Financial Inclusion

This shift wouldn’t be possible without India’s world-class digital infrastructure. Innovations such as UPI, e-KYC, and online brokerages have dramatically lowered entry barriers. Opening bank accounts, verifying identities, and accessing investment products can now be done within minutes, even from smaller towns. This democratization of investing is enabling millions of Indians to participate in the capital markets for the first time.

Rising Incomes, Rising Investments: The New Face of Indian Capital Markets

India’s transformation from a nation of savers to a nation of investors is underpinned by a powerful macroeconomic tailwind: rising disposable incomes.

Per capita income in India has doubled in recent years, growing at a CAGR of 8.3%, outpacing most emerging markets. This surge has expanded the national savings pool from $437 billion in FY14 to $813 billion in FY23. As households accumulate more surplus income, the way they allocate capital is changing—from passive saving to active investing.

An increasing share of this expanding savings pool is flowing into equities and this momentum shows no signs of slowing. While equities currently comprise less than 6% of Indian household wealth (vs. ~22% in the U.S.), the potential for reallocation is massive.

With ongoing regulatory improvements, digitization of financial services, and the rise of low-cost passive investing through ETFs, more Indians are accessing sophisticated investment products with ease. Government-backed initiatives continue to democratize market access, even in semi-urban and rural regions.

As India marches toward its stated goal of becoming a $30 trillion economy by 2047, the role of retail investors will only grow more pivotal. Their capital, conviction, and consistency are reshaping the contours of India’s capital markets—making them deeper, more resilient, and truly representative of the country's economic potential.

As financial literacy further increases and Indians start to participate in the overall growth, financialisation towards higher yielding asset classes is only expected to increase.

%20copy.png)